Tag: risk

-

Global portfolio management

Global portfolio management extends the territorial reach of typical investment strategies, venturing beyond domestic borders to embrace international securities and monetary vehicles. This comprehensive approach is driven primarily by a quest to tap into diversified sources of income and asset classes that show disparate market behaviors, often not correlated with home market movements. International diversification…

-

Portfolio risk calculator and formula

We often say that risk and return are two sides of the same coin. So, when assessing the performance of a portfolio, we need to consider its risk as well as its return. In the previous lesson, we focused on portfolio return. Now, we turn our attention to portfolio risk. Portfolio risk calculator You can…

-

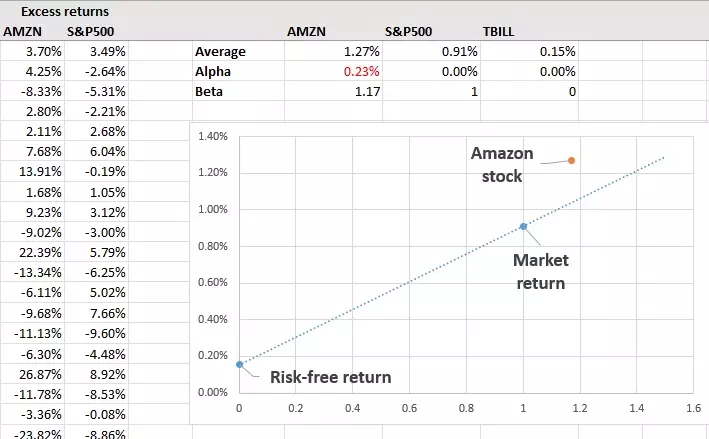

How to calculate Jensen’s alpha in Excel

The purpose of this tutorial is to teach you to calculate Jensen’s alpha in Excel. We’ll estimate the Jensen’s alpha on Amazon (AMZN) shares using the S&P500 as the market benchmark and the 13-week T-bill as the proxy of risk-free asset. Our analysis will be based on five years of monthly data (i.e., 60 observations…

-

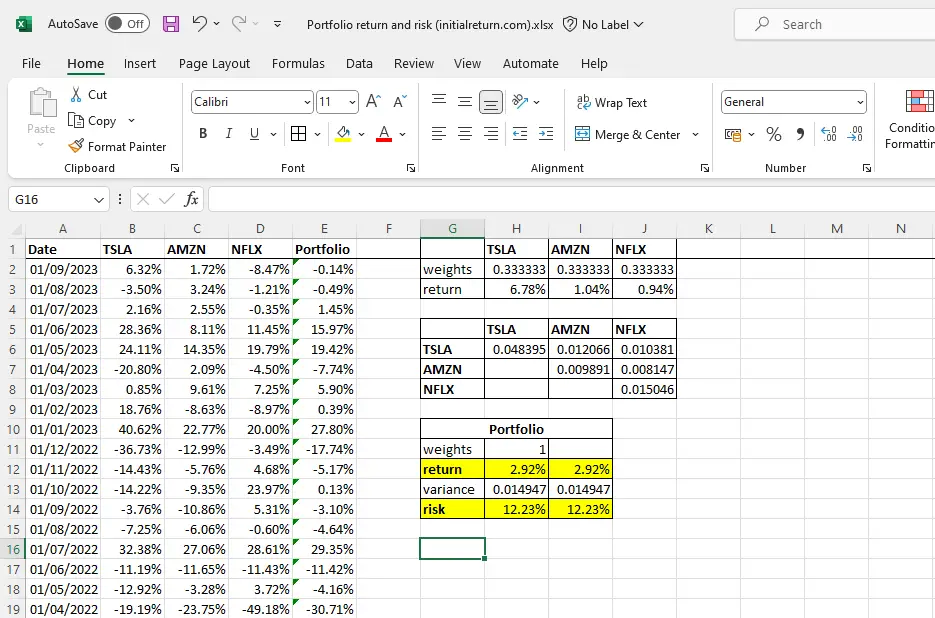

How to calculate portfolio risk and return in Excel

In this tutorial, we’ll teach you how to calculate portfolio risk and return in Excel. We’ll focus on an example where we construct a portfolio of the following three stocks: Tesla (TSLA), Amazon (AMZN), and Netflix (NFLX). If you’re unfamiliar with the formulas for portfolio return and portfolio risk, we’d recommend you check the following…

-

Ambiguity aversion

Many of us might have heard about “risk aversion“, which is a general dislike for risk. But, what is “ambiguity aversion”? To address this question, we need to first distinguish between “risky events” and “ambiguous events”. Let’s do that through a practical example. Imagine a simple coin toss game where you win $1 if the…

-

Psychology of trading

The psychology of trading encompasses the emotional states and moods that traders go through during their trading activities. Emotional trading can have an adverse impact on a trader’s performance, leading to mental issues as well as financial loss. Therefore, all traders should have at least a basic understanding of how emotions influence trading activity. We’ve…

-

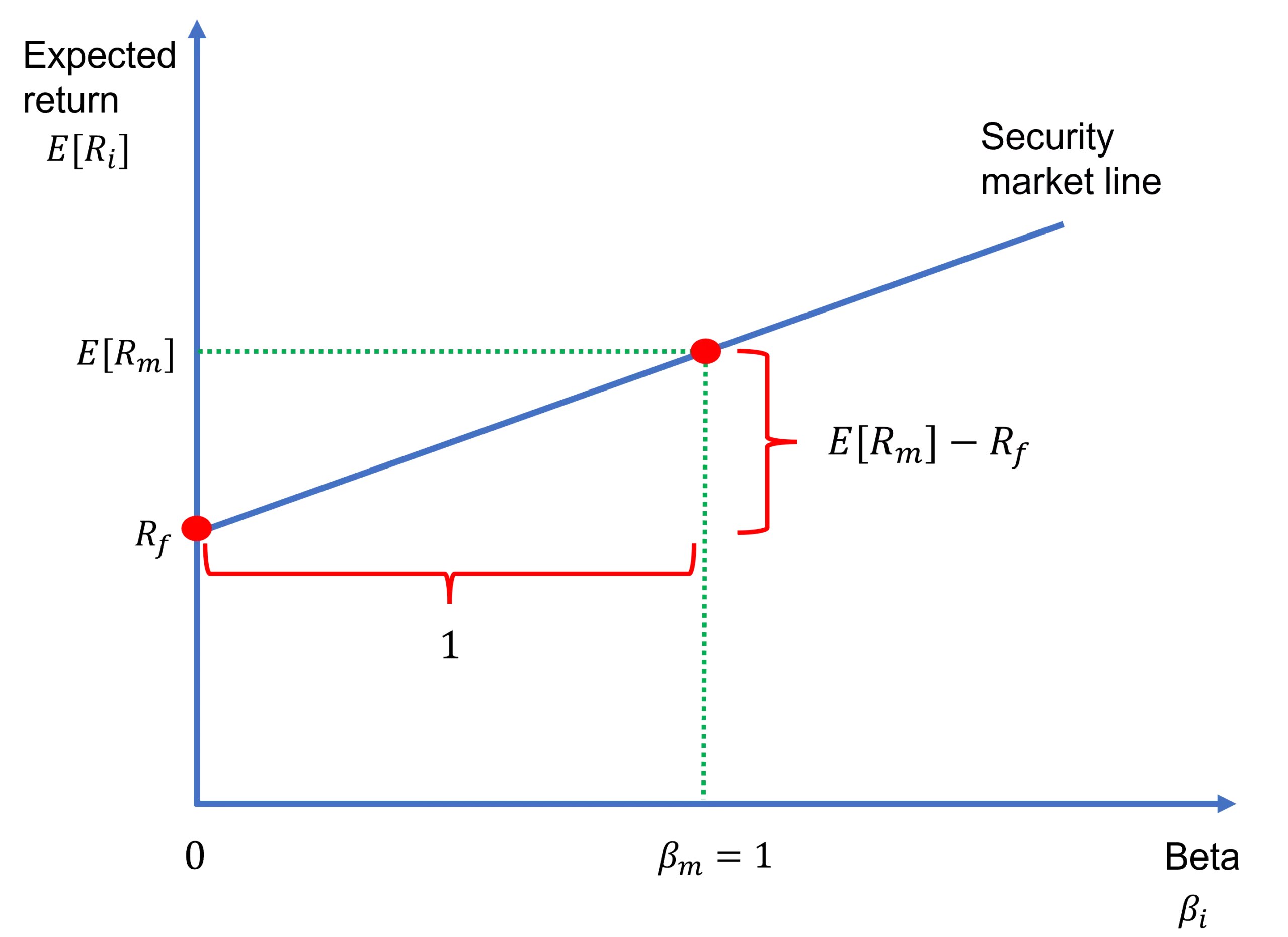

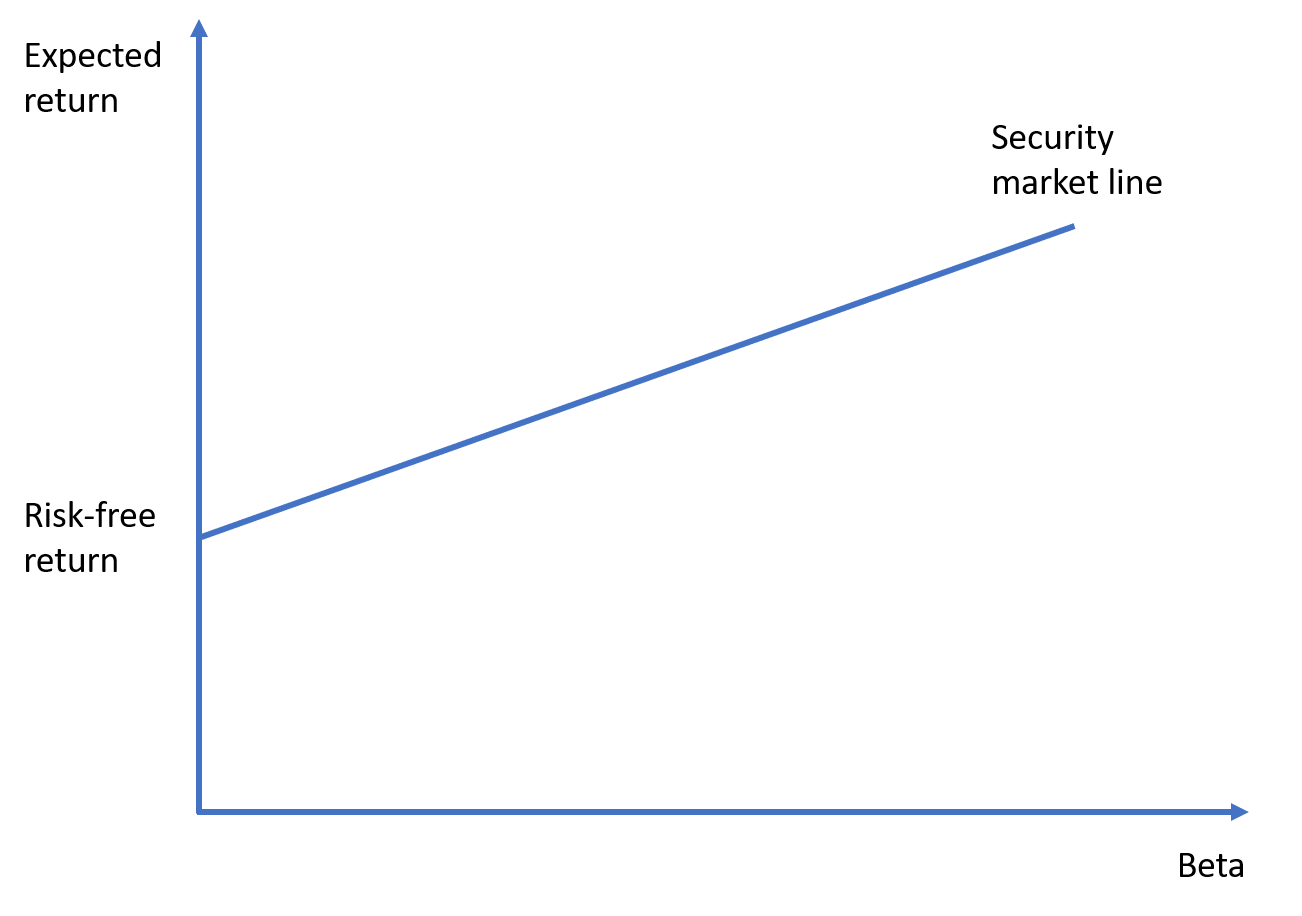

Security market line

The security market line (SML) depicts the linear relationship between expected return and systematic risk, which is measured by beta, according to the capital asset pricing model (CAPM). Specifically, the equation of the security market line is nothing but the CAPM formula: where E[Ri] is the expected return on asset i, E[Rm] is the expected…

-

Capital asset pricing model (CAPM)

The capital asset pricing model (or CAPM) is among the most widely-used asset pricing models by stock analysts and portfolio managers. Its popularity arises from its simplicity and elegance. Analysts and investors can use it to forecast returns or to estimate the cost of equity. In this lesson, we explain this model and its assumptions.…

-

Minimum variance portfolio

In this lesson, we explain what is meant by the minimum variance portfolio (MVP), derive its formula for the two-asset case, and provide an online calculator as well. You can also check out our video tutorial to learn how to find the position of the MVP on the efficient frontier using Excel’s solver tool. And,…

-

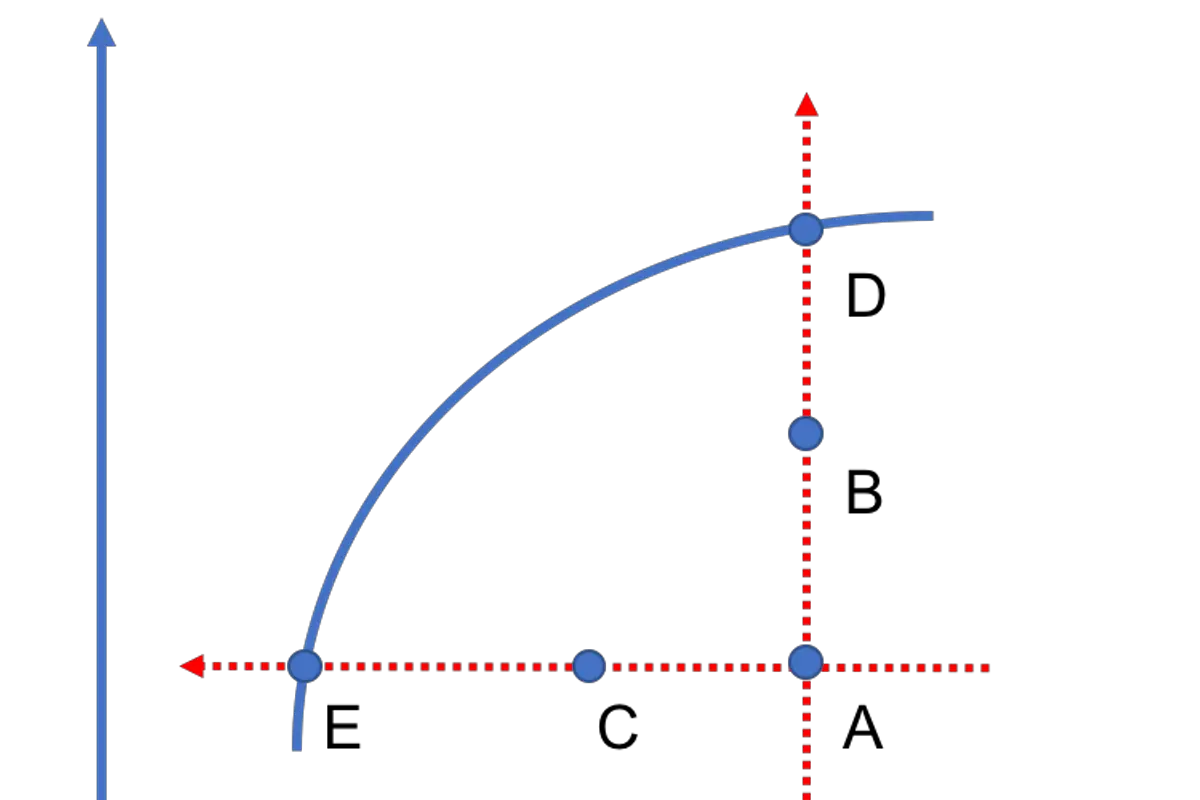

Efficient frontier calculator

In modern portfolio theory, the efficient frontier represents the collection of all efficient portfolios within a market. Efficient portfolios offer the best risk-return tradeoff and, as such, are superior to inefficient portfolios, which are suboptimal. In this lesson, we explain how investors can trace the efficient frontier using mean-variance optimization (the topic of the previous…